Episode #372: Mastering Financial Conversations, The Key to Reducing Insurance Dependence with Linda Anderson

Listen Now

Are you scared to drop PPO plans for fear of losing your income? Your fear is valid! But do you know that staying in the PPO network negatively impacts your income? You can learn more about this in today’s episode!

In this episode, Gary and Naren talk about the change in your income when you decide to drop PPO plans. He also discusses a real-life case study from his coaching program. Finally, Gary provides the listeners with an actionable checklist to identify if they are ready to drop PPO plans.

www.lessinsurancedependence.com/mastering-dental-marketing/

Naren: Hello everyone. Welcome to the less insurance dependence podcast the official podcast of the reducing insurance dependence academy www.rid.academy. Please consider this an invitation to become a member of RIDA as a gift from us in appreciation for your listenership. This is Naren, your co-host. Today’s topic is, will my income go down when I drop PPO plans. Will my income go down when I drop PPO plans? Before we get into today’s topic, I have a quick announcement. Gary’s master class is coming up on the 28th of July from 7 to 10 pm eastern time. It’s a Thursday. 28th of July the topic is the 2.5-million-dollar practice model, the 2.5-million-dollar practice model. We give three hours of CE and here Gary literally will lay out how do you build a 2.5-million-dollar practice, how do you structure it, what are the key success factors and how do you kind of orchestrate this. Gary any, any, thoughts?

Gary: Yeah, I’m really excited about that upcoming master class. It’s, it’s, one of my favourites when I look at the, the, menu of titles we have in our master class series this is certainly one of my favourites and I will literally just break it down step by step of all the details around that 2.5 million practice, and well there’s many practice models. This is one that may serve as a guide for you. It may be one that says hey I like that because actually if you follow our guidance on this, that’s a model that can help you develop a thriving practice, which the definite my definition of a thriving practice, is one that provides personal professional and financial satisfaction. And that’s a model that can certainly apply that can allow you to achieve that, for sure and I’ve had the privilege of helping many, many, many, of our clients get to that level of practice performance and have seen the results and the results are consistent, it’s a really great practice model not, not, that there aren’t other good practice models but that’s a really good one. So, hey, come join us on, July28th and maybe that will give you all the details you need to sort of pin that practice model on your goal list, and I would love to see you at that master class. It’s, it’s, live stream so it is virtual meaning you can attend from the comfort of your home or office so no travel inconvenience or cost however it’s live so you can ask me questions and make it more interactive and love to have you come join us. Three hours allows me to take a deep dive into a specific topic and that topic will be the 2.5-million-dollar practice model

Naren: Thank you Gary and the topic today will my income go down when I drop PPO plans, it came from a webinar Gary did recently on the topic of six steps to reducing insurance dependence. So, you know Gary does this webinar and at the end we you know people ask questions and there was this question, literally word for word you know the doctor I guess was afraid of her income going down, if she followed through and started reducing insurance dependence. So, she literally blurted it out you know

Gary: and I think she typed it in the Q and A panel

Naren: yes

Gary: she did and then if I correct me if I’m wrong but I think yeah you were on the panel and you were helping moderate that webinar

Naren: Yes

Gary: and you saw that come in and of course the q and a panel is public everybody attending can see those questions

Naren: yes, and I think what happened was a bunch of other people chimed in like hey I want to know about this too

Naren: absolutely and I think I, I, if I missed if I’m not mistaken like quite a few people wanted the answer

Gary: yeah

Naren: because what they were asking Gary is you have done this for so many years have you seen anybody’s income go down you know after they decide to reduce insurance dependence right?

Gary: Let me let me answer the question you know, let me answer the question just point-blank right here and then we’ll talk more about it. You know, is it possible that when you resign from PPO plans that your, yourincome could go down and the answer to that question is yes, that’s certainly a possibility. I’ve just never seen it happen. Now that doesn’t mean it couldn’t happen, I guess you know if, if, if, you did everything wrong and you know simply didn’t have the circumstances in your practice that would you know even allow you to consider that, then yeah possibility of your income going down. I’ve just never seen that happen in my coaching work. I’ve never, never, seen that happen. That’s a fear and I get the fear. The fear of that is well Gary I already feel like my budget’s pretty tight most, most, dentists on PPO plans feel like they’re not making enough income

Naren: Yes

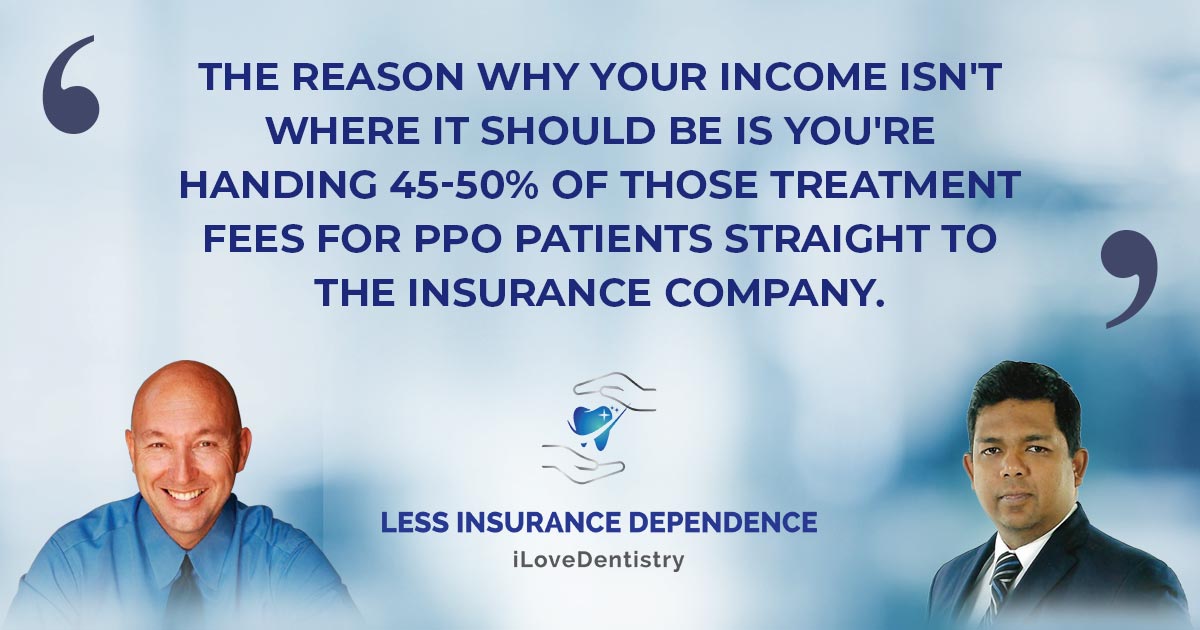

Gary: and the reason is they’re handing 45 to 50 off to the insurance company so it’s pretty uniform that I’m already making I’m already not making much money, it’s all relative it’s not like you’re in the soup line or anything

Naren: yeah

Gary: but it’s like hey I’m not making much money and I couldn’t remotely afford to have it go down and if I drop plans is it going to go down so I it’s like I’m already underfunded with my income

Naren: yes

Gary: and if it goes backwards it’s going to be worse and I don’t want that

Naren: I would rather stay where I am than take that risk

Gary: right, I’d rather you know deal with the devil I know than the devil I don’t know

Naren: right

Gary: and the reason why your income isn’t where it should be is that you’re handing 45 to 50 percent of those treatment fees for PPO patients straight to the insurance company

Naren: So, let me ask you some follow-up questions Gary, you said you have never seen that happen in your coaching work

Gary: no and in fact if you look at this for just a minute and I I just want you to run, run, the, the, math through with me if you’re a listener on this. One of our goals when you drop PPO plans is to keep as many of your existing patients as possible, as many of your existing patients as possible. Recently I’ll use an actual case study without using the name, because I don’t want, I don’t want to create any HIPPA violations of confidentiality. A client did this and he kept 88 percent of his in-network patients’ 88 percent. Now would you agree that’s a pretty darn good end result

Naren: yeah, absolutely Gary

Gary: By the way he was ecstatic. He was ecstatic about that because he said I thought I’d lose way more I thought

Naren: I know you tell people they could lose 10 to 15 percent right, so this person is kind of on the high end meaning they did really well

Gary: Yeah, they did well. He kept 88 percent, and lost 12 percent of his patients. So now run that in reverse that means he is getting a hundred percent of his fee on 88 percent of his patients

Naren: right

Gary: 100 percent of his fee on 88 of his patients okay. Now, the alternative was when he was in network his average adjustment was 45 percent. Now not 100 of his practice was PPO. So, I need you to do some sophisticated math for me on this one Naren, 80 percent of his practice was PPO. So, on 80 percent of his practice, he’s getting 55 percent of his fee

Naren: right

Gary: So, he’s so 80 percent of his patients he’s getting 55 percent of his fee and on 20 percent of his practice, he’s getting a hundred percent of his fee. So, blend those two and run the math to tell me what his overall percentage of, of, income was based on the fact that 80 of the patients you know are PPO patients he’s only getting 55 percent of his fee and, and, then on the remaining 20 he’s getting 100 percent of his fee. What does that look like?

Naren: Yes, so if I were to compare the two, the one who kept 88 percent but collected a hundred percent of the fee think of it like he’s collecting 880 000 dollars. I just want to use some round numbers okay

Gary: well, give me percentages give me percentages

Naren: percentage, one is collecting 88 percent

Gary: 88 percent, and all that is is 100 of your patients or 80, 80, 88 percent of your patients are now paying 100 percent of your fee

Naren: Yeah

Gary: multiply that out that’s 88 percent

Naren: 88 percent

Gary: We have another way

Naren: other one, when I did the blended math, he’s only instead of keeping 88 percent of the money he’s only keeping 64 percent of the money. So, in other words even after blending it, 36 percent goes to insurance companies

Gary: so blended, you have to blend it

Naren: Yeah

Gary: because the truth was not 100 percent of his patients were PPO

Naren: right

Gary: but you know but it was 80 percent of his patient and then 20 percent, so that blended percentage was he was getting 64 percent of his fee

Naren: Yes

Gary: yeah, but that’s not the end of the equation, that’s not the end of the equation. That by itself

Naren: even if it’s the end of the equation, one guy is making 88 percent the other guy is making 64 percent so he’s better off

Gary: if you’re a listener we’re asking you

Naren: yeah

Gary: would you rather get 64 percent of your fear or, or, or, 88 percent. Take as long as you like.

Naren: Right

Gary: 64 last time I checked even with the new math Naren, 88 percent was better than 64 percent. Does that make sense?

Naren: yes, yes,

Gary: so, I have to answer the question very specifically, in my coaching work I have never seen anyone go backwards in their income I’m not saying could it happen you bet

Naren: right

Gary: if you were to do this in a cavalier way, without the preparation without any training to your team without really you know putting some effort into it, sure that can happen but that’s none of our listeners, never, you’re listening to this to learn how to do it right

Naren: Right

Gary: That’s what happened to you and furthermore it’s never happened in my coaching work, never happened. It’s always gone up. Look just do the math do the math it goes up

Naren: right

Gary: it goes up you know and, and, your income goes up as it should be and your overhead goes down because you don’t have to your overhead is built on the top number of how much you have to produce, not the amount of money you’re able to collect,

Naren: Right

Gary: and so, there’s another more complicated calculation goes in there is that your overhead actually goes up, your income could stay the same, if, if, you know we’ve never seen that happen you know in terms of that low of a result, but you’d still be better off financially, because now your overhead is less because your gross production is less, but the answer is I’ve never seen it happen it could happen but I’ve never I’ve never seen that happen. Now if I want to make this actionable, how can you check the pulse of your practice to see if you’re ready you know just to see if you’re ready, how could you check that. I would point you to two of our six steps to successfully drop PPO ones I point to two. The first place I point to is how relationship driven is your practice. How much do you connect with your patients? Do we know their names or spouses’ names or kids’ names do we know the dog’s name do we know their hobbies do we do we know their interests do we know what’s going on with their life and do we connect with them on their visits to our office, and how would you rate that arbitrage this is very subjective? How would you score your practice performance using say an elementary grade school teacher grading scale A B C D or F. I doubt that any of our listeners would be in the D or F category if you are going back and listen again

Naren: yes

Gary: But if you objectively look at this and you say well, I think we’d do pretty well but we could do better maybe we’re a B plus maybe we’re an A minus then figure out what you can do to do better on connecting with your patients. One of the things you can do is make sure you have a place in your computer, where you and your team enter personal information with your, about your patients. Make sure your team members enter information and then yourself doctor come in early before your morning huddle come in 20 minutes before your morning huddle and read those electronic note cards to prepare for your day and that way when you see your patients in hygiene you can connect with them Gary it’s good to see you how’s your wife Therese how’s your yoga studio how’s your grandson Kannan. That’s the kind of information that will be on the card. I always say that if you don’t actually care about your patients don’t do this but again, I don’t think that applies to any of our listeners. They care about their patients; you know make sure your team members and information because maybe someone will say hey Linda ran you know the phoenix marathon last week and you can ask Linda about her marathon experience. Hey Linda, was thinking about you last week, how did you do the marathon or maybe you know that she placed second in her age category. You say congratulations how would that be imagine that Naren, your patient’s name’s Linda doctor comes in its Linda it’s so good to see you. Hey, one of the things I was happy about seeing you today is I saw your second place finished in the marathon last week, way to go. Would you say that’s connecting with a patient?

Naren: absolutely

Gary: absolutely, so the two things I would work on if you feel like you know hey I, I, want to, I, I, I, want to make sure that my income doesn’t go backwards when I drop plans, work on strengthening the relationship driven aspect to your practice, and, and, we could go on for hours about all the different things you could do but just get an idea here and the second thing I would do is I would proactively replace any patients that you might lose, remember our example, he lost 12 percent of his patients

Naren: yes

Gary: but it was no problem because he had proactively replaced them by digital marketing, he had proactively replaced him and he became an EKWA client and you replaced those patients in abundant more, more, than that. So, you not only have to replace the ones you lose, but you have to replace the flow that would historically have come in from that plan, and he did that and did it proactively. So now he was in a position of strength going on so there’s two actionable things you can do so you don’t just sit here and say well I’m going to roll the dice and see what happens I hope my income doesn’t go backwards. Now don’t do that, but actually take steps to ensure that it doesn’t and there’s two steps we just went through today there. Maybe you could put a link to the marketing strategy meeting with, with, Lila any of our listeners would like to find out how you can help their practices like you help ours, life smiles but also how you help our clients I refer our clients to you and I see the fantastic results with all my clients as well. So, it’s not like we’re a one-off it’s not like you’ve rocked it with us but belly flopped with all the other clients that’s not it at all. I see it time and time and time again. It’s EKWA, www.EKWA.com, forward slash msms and it stands for marketing strategy meeting. Well, hey I I’m glad you asked the question Naren, I’m glad you were on the panel that saw that question you not only saw the question but you saw the, the, interest around it, it wasn’t just coming from one doc. I’ve always said be sure to ask questions because you’re not the only one thinking it

Naren: Yes

Gary: and that was an example for sure because one person was brave enough to type in the question but I think a bunch of other people jumped in and said you know me too, mee too, I want to know this too

Naren: okay I have two follow-up quick questions

Gary: Pleas

Naren: one is you said during the webinar that there are few people you told them they are not ready to reduce insurance dependence. In other words, if they do, they might see their income go down

Gary: yeah, don’t do that

Naren: Can you explain that explain I’ve had to do that I can count on one hand the number of times I’ve had to do that. I don’t like delivering that message because you know it’s not the direction, I want that practice to go, but I also have a professional obligation to serve the clients. No, you shouldn’t do this you’re it’s not that you couldn’t ever do it but you’re not ready and the bottom line was, these practices were not giving their patients tangible reasons for people to come to them and it would be any different than if they went to the clinic next door and I’m using the word clinic in a negative way you know the doc and the, the, dentist in a box and we talk about doc in the box

Naren: Right

Gary: You know for medical care but you know there’s versions of the dental dentist in a box. They weren’t doing anything differently that would set their practice apart then the, clinic that just processes people next door, and, and, every time I’ve had to deliver that message which again, I count on one hand the doctor has said yeah that’s I that’s my feeling too. You’re not telling me something I don’t already know Gary but you’re confirming something that I felt myself and then I said it’s not that you couldn’t ever do it but you can’t do it from where you are right now

Naren: The second question I have is you know we have mutual clients and I have seen the opposite happen, like my experience is a minimum hundred thousand more they’re taking home and sometimes it’s three hundred thousand more. Can you explain how that happens?

Gary: Well, we’ve actually seen radical improvement in you know in pre-tax income from the doctor, you know because well you know think about. If, if, you stop giving away that money to the insurance company, stop giving that away where does it go to it goes right to the bottom line. You already spent all the expenses to generate the dentistry

Naren: right

Gary: So, if you have an office that has seven hundred thousand dollars’ worth of adjustments and by the way that’s not some crazy number. That’s numbers that we see

Naren: Right

Gary: and you stop giving that 700 away, a strong portion of that you know even if you lose 12 percent of those patients

Naren: Yeah

Gary: a strong percent of that’s going to go directly remember that increased income goes right to your bottom-line profitability because you already generated all your expenses to create that dentistry. You already paid your team, you paid the supplies, you paid the lab fused outside lab you, you, paid all the technology costs you, you, paid for everything and now it just goes to you. So, we often see astounding increases in income when you stop. I mean hey, would your bank account be better let’s say you write off 500 000 a year. I’m making up a number

Naren: right

Gary: an insurance adjustment would your bank account be better if you stopped giving that 500 000 take as long as you like it

Naren: has to go somewhere and it goes into your bank account.

Gary: It goes into your bank account which is where it should go. Now maybe not the entire 500 but a majority of it could.

Naren: yes exactly

Gary: yon know and so but it’s not incremental increases. So, income doesn’t go up from say I’ll make up numbers 150 to 160.

Naren: right

Gary: You know it goes from 150 to 320.

Naren: exactly right

Gary: yeah, you’re in a different tax bracket at that point

Naren: Yes

Gary: well, hey I hope this has been inspiring so to answer the question will my income go down when I drop PPO plans and the candid direct answer is it’s entirely possible but if you do it right, I’ve not seen that happen I’ve never seen that happen I hope that’s encouraging to all of you. Hey Naren, thanks for your support of this podcast. Thanks for all you and your team do at EKWA to support not only life smiles but all of our clients as well I also to thank our listeners thank you so much for the privilege of your time. Naren and I look forward to connecting with you on the next less insurance dependence podcast

One of Gary's most significant achievements as a dental practice management coach is transforming his own practice, LifeSmiles, from one that was infected with PPO plans, no effective marketing strategy, and an overhead of 80% to a very successful dental practice that is currently one of the top-performing practices in the US.

One of Gary's most significant achievements as a dental practice management coach is transforming his own practice, LifeSmiles, from one that was infected with PPO plans, no effective marketing strategy, and an overhead of 80% to a very successful dental practice that is currently one of the top-performing practices in the US.

As CEO of Ekwa Marketing, Naren has over a decade of experience working with dental practices and helping them attract the ideal type of patients to their practices. It is his goal to help dentists do more of the type of dentistry they love with the help and support of effective digital marketing.

As CEO of Ekwa Marketing, Naren has over a decade of experience working with dental practices and helping them attract the ideal type of patients to their practices. It is his goal to help dentists do more of the type of dentistry they love with the help and support of effective digital marketing.